All Categories

Featured

Table of Contents

The are entire life insurance policy and universal life insurance policy. The cash money value is not included to the fatality advantage.

After ten years, the cash money value has expanded to roughly $150,000. He takes out a tax-free finance of $50,000 to begin a business with his brother. The plan loan rate of interest is 6%. He pays back the lending over the following 5 years. Going this path, the interest he pays goes back into his policy's cash value rather of a banks.

Picture never ever needing to fret about small business loan or high rate of interest prices once more. What if you could borrow money on your terms and develop wide range concurrently? That's the power of infinite banking life insurance policy. By leveraging the money value of whole life insurance IUL plans, you can expand your riches and borrow cash without counting on typical banks.

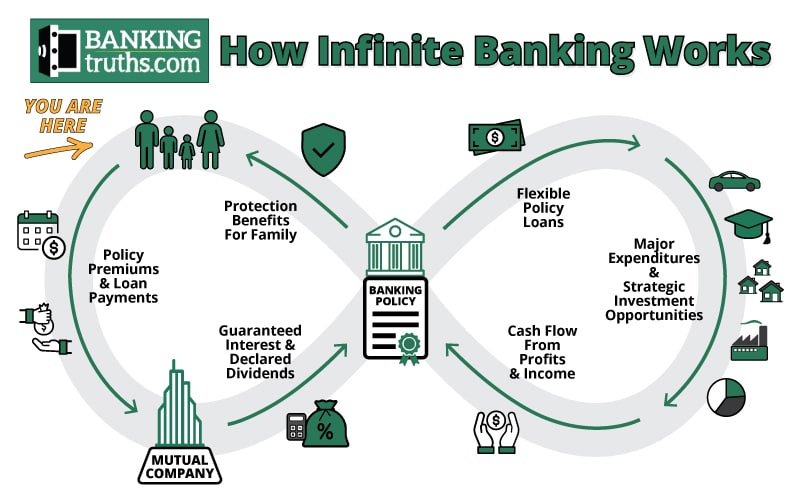

There's no set funding term, and you have the liberty to determine on the payment schedule, which can be as leisurely as settling the funding at the time of death. This versatility reaches the maintenance of the fundings, where you can go with interest-only payments, keeping the funding balance flat and convenient.

Holding money in an IUL taken care of account being attributed rate of interest can commonly be much better than holding the money on down payment at a bank.: You've always fantasized of opening your very own bakery. You can borrow from your IUL plan to cover the initial costs of leasing a space, buying devices, and employing staff.

Be Your Own Banker Whole Life Insurance

Personal fundings can be obtained from conventional banks and credit unions. Obtaining money on a credit history card is normally really costly with yearly percent rates of rate of interest (APR) frequently getting to 20% to 30% or even more a year.

The tax therapy of policy fundings can vary substantially relying on your nation of house and the details regards to your IUL policy. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, plan finances are typically tax-free, supplying a considerable advantage. However, in various other jurisdictions, there might be tax implications to think about, such as prospective taxes on the funding.

Term life insurance just gives a survivor benefit, with no cash value accumulation. This implies there's no cash worth to obtain versus. This write-up is authored by Carlton Crabbe, Principal Executive Policeman of Funding forever, a specialist in giving indexed universal life insurance policy accounts. The information offered in this article is for educational and informational objectives just and must not be construed as economic or financial investment recommendations.

Family Banking Strategy

When you initially listen to about the Infinite Financial Concept (IBC), your very first response may be: This sounds too excellent to be true. The trouble with the Infinite Banking Principle is not the principle however those individuals using a negative review of Infinite Financial as a principle.

As IBC Authorized Practitioners via the Nelson Nash Institute, we assumed we would certainly answer some of the top concerns people search for online when learning and comprehending whatever to do with the Infinite Banking Principle. So, what is Infinite Banking? Infinite Banking was created by Nelson Nash in 2000 and completely clarified with the publication of his publication Becoming Your Own Lender: Open the Infinite Financial Idea.

How To Become Your Own Bank

You think you are coming out economically ahead because you pay no rate of interest, yet you are not. With saving and paying money, you might not pay passion, however you are using your money when; when you spend it, it's gone for life, and you give up on the possibility to earn life time compound interest on that money.

Even financial institutions use whole life insurance policy for the very same functions. The Canada Profits Agency (CRA) even identifies the value of taking part whole life insurance coverage as an one-of-a-kind property class utilized to generate lasting equity safely and naturally and provide tax obligation advantages outside the scope of standard investments.

Be My Own Bank

It allows you to produce wide range by satisfying the banking feature in your very own life and the ability to self-finance major way of living acquisitions and expenses without disrupting the substance interest. One of the simplest methods to consider an IBC-type participating whole life insurance policy plan is it approaches paying a mortgage on a home.

Gradually, this would certainly create a "continuous compounding" result. You understand! When you obtain from your taking part entire life insurance policy policy, the money value proceeds to grow nonstop as if you never ever borrowed from it to begin with. This is due to the fact that you are using the money value and survivor benefit as collateral for a car loan from the life insurance policy business or as security from a third-party lender (referred to as collateral lending).

That's why it's critical to deal with a Licensed Life Insurance Broker accredited in Infinite Banking that structures your taking part whole life insurance policy policy appropriately so you can stay clear of unfavorable tax obligation ramifications. Infinite Banking as an economic method is except everybody. Right here are a few of the advantages and disadvantages of Infinite Financial you need to seriously think about in deciding whether to move on.

Our favored insurance provider, Equitable Life of Canada, a shared life insurance coverage firm, specializes in participating entire life insurance policy plans specific to Infinite Financial. In a shared life insurance coverage company, insurance policy holders are considered company co-owners and receive a share of the divisible surplus produced annually through dividends. We have an array of providers to select from, such as Canada Life, Manulife and Sunlight Lifedepending on the requirements of our customers.

Please additionally download our 5 Leading Questions to Ask A Boundless Financial Representative Before You Employ Them. For even more information about Infinite Banking browse through: Disclaimer: The product offered in this newsletter is for informational and/or academic purposes just. The info, viewpoints and/or sights shared in this newsletter are those of the authors and not always those of the distributor.

Rbc Visa Infinite Private Banking

The principle of Infinite Banking was developed by Nelson Nash in the 1980s. Nash was a finance expert and fan of the Austrian college of business economics, which supports that the value of products aren't explicitly the outcome of typical economic structures like supply and demand. Instead, people value cash and products in a different way based upon their economic status and demands.

One of the pitfalls of standard financial, according to Nash, was high-interest rates on financings. Also several individuals, himself included, got right into monetary problem due to reliance on banking organizations.

Infinite Financial requires you to own your financial future. For ambitious people, it can be the very best monetary tool ever. Here are the advantages of Infinite Financial: Arguably the solitary most valuable facet of Infinite Banking is that it improves your cash flow. You do not require to undergo the hoops of a conventional financial institution to obtain a car loan; merely demand a policy funding from your life insurance company and funds will be provided to you.

Dividend-paying entire life insurance is really low threat and provides you, the insurance policy holder, an excellent bargain of control. The control that Infinite Financial offers can best be organized into two groups: tax benefits and asset defenses.

Entire life insurance policy policies are non-correlated properties. This is why they function so well as the monetary structure of Infinite Banking. No matter what takes place on the market (stock, property, or otherwise), your insurance coverage policy preserves its well worth. A lot of people are missing this vital volatility buffer that helps protect and grow wide range, instead breaking their cash right into 2 containers: financial institution accounts and financial investments.

Market-based investments grow riches much faster however are exposed to market fluctuations, making them naturally high-risk. What if there were a 3rd pail that provided safety however likewise modest, guaranteed returns? Whole life insurance is that third container. Not just is the price of return on your entire life insurance policy policy ensured, your survivor benefit and costs are also assured.

How Infinite Banking Works

This framework straightens completely with the principles of the Continuous Riches Approach. Infinite Financial attract those seeking higher financial control. Right here are its major advantages: Liquidity and availability: Policy fundings offer instant access to funds without the restrictions of typical small business loan. Tax efficiency: The cash value grows tax-deferred, and policy car loans are tax-free, making it a tax-efficient device for constructing riches.

Possession protection: In several states, the money value of life insurance policy is shielded from lenders, adding an additional layer of economic safety and security. While Infinite Financial has its merits, it isn't a one-size-fits-all option, and it comes with substantial drawbacks. Here's why it may not be the most effective method: Infinite Banking typically calls for intricate policy structuring, which can perplex policyholders.

{kind=link}

Latest Posts

Infinite Banking Course

Be Your Own Bank Whole Life Insurance

Nelson Nash Becoming Your Own Banker Pdf